The affordability squeeze in housing shows no sign of easing – on the contrary, rents and prices continue to rise and have exceeded income growth in recent years. Analysis for Dublin City Council as it formulates its development plan from 2022 to 2028, much of it undertaken by KPMG, highlights some of the key issues over the years ahead.

It shows challenges for renters and purchasers continuing and a growing group who earn too much to qualify for social housing but do not earn enough to either buy or rent in the market – including many couples with two decent incomes.

In the light of this, new research from the Banking and Payments Federation of Ireland (BPFI) shows the increasing role of the " Bank of Mum and Dad" in getting some buyers over the affordability gap. It looks as is this reliance on family assistance is here to stay – and the State is now stepping in as well.

1. Future forecasts:

Local authorities need a basis to plan and a common basis for forecasting has been developed, with KPMG Analytics hired by Dublin City Council (and some others) to develop forecasts.

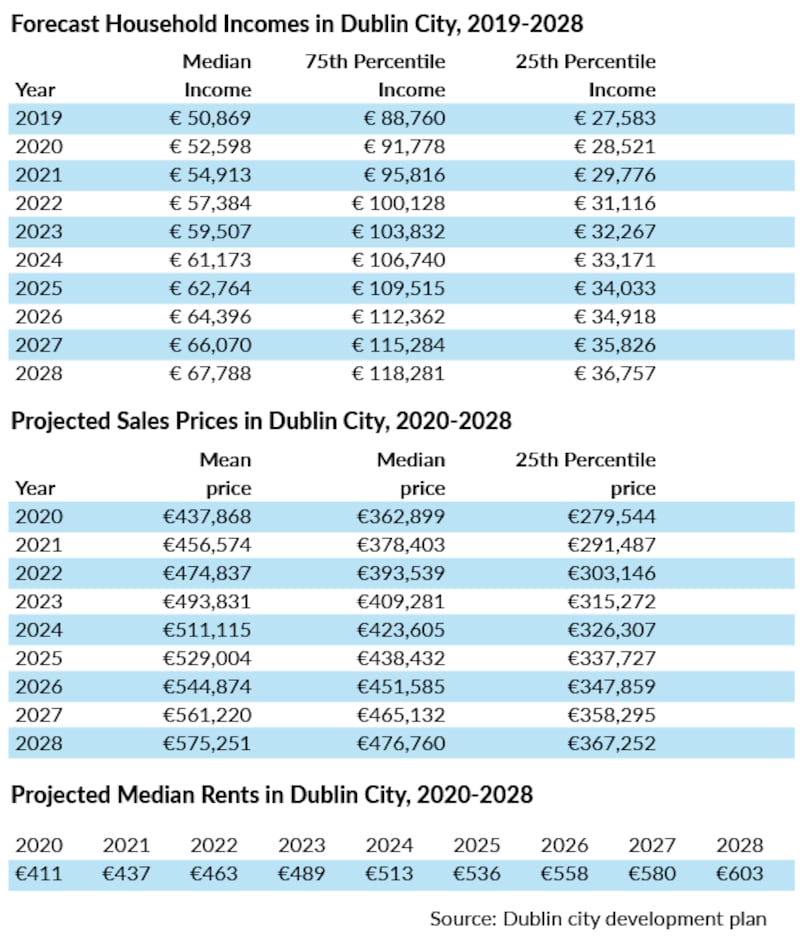

To judge affordability, you need to forecast incomes, property prices and rents – and of course availability of appropriate properties to rent or buy are also crucial. It is important to recognise that forecasts are only as good as the assumptions they are based on and we are facing into a period of particular economic uncertainty.

The predictions indicate that affordability for both buyers and renters could continue to worsen. Property price growth between this year and 2028 is predicted to be 26 per cent, bringing the median price in Dublin City to just under €477,000. (The median is the average calculated as the number at the mid-point if all property prices are listed from the dearest to the cheapest – it thus is not overly influenced by a few really expensive houses)

Over the same period, the median income is expected to rise by just under 23.5 per cent to €67,788. So affordability for purchasers, already stretched, would be a bit worse.

With average rents expected to rise by 38 per cent by 2028 to over €600 a week, or over €2,600 a month, rental affordability would get significant worse. Given that rents here are already at record levels and are high by EU standards, this is a big social challenge and also a key threat to economic competitiveness.

There are complex assumptions here about housing availability and households who can’t buy deciding to rent and so on. But the overall trend is interesting.

Because household incomes are rising, more households will exceed the €35,000 threshold for social housing provision. So, even adding in the need to house those currently homeless, the percentage of “new” households needing social housing falls from 40 per cent of the total in Dublin City in 2021 to just over 35 per cent by 2028.

By contrast those facing what is called an “affordability constraint” – they can’t afford to buy or rent in the market – rises from 26 per cent now to 32 per cent. And this does not count the frustrated buyers currently living with parents.

The rest – around one third – are calculated as being able to afford to rent or buy. This means you have to be in the top third of earners to afford to buy or rent in the open market in Dublin city. Detailed estimates for the populations of Dublin 1 and Dublin 8 underline this point.

Of course, the real world could work out differently over the next few years. Who knows what will happen to the economy, incomes or property prices? But the data underline two key points – the difficulty for even middle income households of earning enough to buy or rent in the current market, and the increasing prevalence of what we might call the “squeezed-out middle” – those who earn too much to qualify for social housing, but not enough to survive in the open market.

These people will rely on the building and supply of affordable homes, or on the rental models such as cost rental which involve an element of State subsidy to ensure affordability. The new Government housing plan proposes to increase the supply in both areas, but the challenge is immense given the scale of the problem.

Dublin City has its own particular characteristics of course – but the same issue is repeated in the big urban housing markets across the State.

2. The bank of Mum and Dad – and the bank of the State:

To try to bridge the affordability gap, increasing numbers of buyers are relying on gifts of loans from their parents. With an average/median deposit of €52,100 for a first-time buyer, according to the BPFI figures, it is no wonder some help was needed, particularly for those already paying sky-high rents and thus finding it impossible to save.

The total equity put into purchases by first-time buyers in the first half of this year was €636 million, of which €393 million was their savings and €149 million was gifts, most likely coming from parents or close relatives. The other €94 million was mainly Help-to-Buy refunds of tax along with some inheritance money.

In a comment on the figures, Davy Stockbrokers chief economist Conall MacCoille pointed out the the gifts or loans from “the Bank of Mum and Dad” were equivalent to a very significant 6 per cent deposit on the €2.2 billion of mortgage lending to first-time buyers in the first half of the year.

With Ireland’s household savings rate of 29 per cent in the first half of 2021, it isn’t surprising that parents are passing on some savings to their children, MacCoille said, though clearly the pandemic has also adversely affected a significant number of households.

Karl Deeter, of Irish Mortgage Brokers, said family gifts and loans contributed more cash to home purchases than a number of the smaller niche lenders. Given rock bottom interest rates on savings , the incentive to give the money to family to help them buy a home was all the greater, he said.

Now the State is to step in as well via a shared equity scheme known as the “first-home” scheme. That will involve the State taking an equity stake of up to 30 per cent in a new home bought by a first-time buyer (there may be some allowances for separated couples as well).It is due to kick off early next year and full guidelines are not yet available,

The scheme will require the applicant to take out the maximum bank loan – 3.5 times income – and will then bridge the gap to allow a purchase to take place. There will be a property price cap – the indication is €455,000 in the most expensive areas – and the maximum State equity will be cut to 20 per cent in cases where the buyer also avails of the Help-to-Buy scheme, which effectively offers a tax refund equal to up to 10 per cent of the purchase price to a maximum of €30,000 up to the end of 2022. ( After that it is due to revert to a cap of 5 per cent or a maximum of €20,000 in cash)

3. The squeeze:

The Help-to-Buy and shared equity schemes to help people close the affordability gap have been criticised as adding to demand – and thus prices. This has led to significant scaling back of the initial plans for the shared equity scheme.

Much, of course, will depend on the supply of houses and apartments and the price at which they are available. Here the cost of building in Ireland, particularly of apartments, remains a key blockage.

There are signs of a pick-up in building, with the BPFI analysis pointing to a rise in housing commencement. On an annualised basis, more than 30,500 units were commenced in the 12 months to end-September 2021, the most in any 12-month period since the period ending in August 2008. This should mean completions rise sharply next year from this year’s expected 22,000, though increased numbers of apartments – which take longer to build – make exact forecasts difficult.

But, for now, prices and rents are heading higher and big questions remain about affordability in the years to come. Significant State investment is now inevitable: the debate is over how much can usefully be spent and where it can be directed. And as well as the challenge of social housing, helping those squeezed in the middle of the market will be a big challenge. Designing building plans and supports to help this group is a complicated – but vital – task.