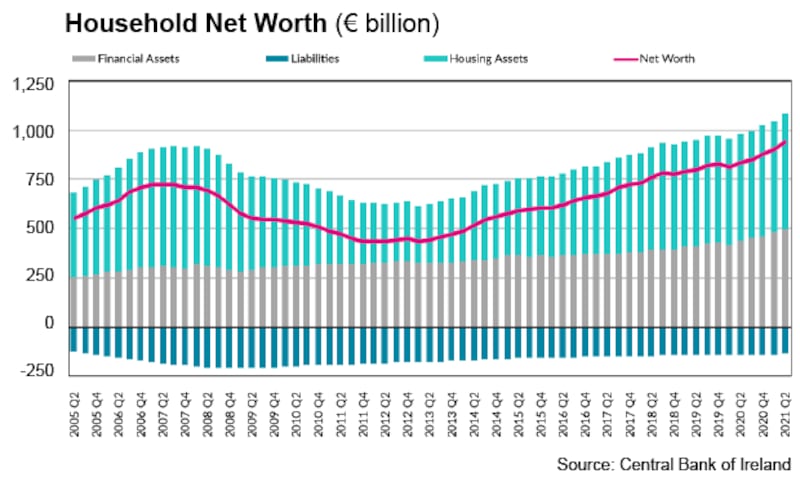

If Irish household wealth keeps increasing at current rates, it will exceed €1 trillion in 2022. In the middle of this year, thelatest Central Bank figures showed that net wealth – households' assets minus borrowings – stood at €935 million, exactly €100 million higher than one year previously and more than €125 million above pre-pandemic levels. This equates to €186,589 per capita, though as the Central Bank points out, this says nothing about the distribution between households.

Covid-19 has hit some parts of the economy hard, but rising house and share prices – and the lack of ability to spend normally during lockdowns – have boosted overall wealth significantly. The additional cash savings may, of course,be transitory. Property is still the bedrock of Irish wealth, but other investments are increasing important. Let’s see the key trends.

1. The housing effect

Back before the financial crash, Irish households held gross housing assets valued, at the price peak in late 2007, at around €610 billion. Total wealth at the time was just over €700 billion. It was all about property. Total household borrowings, most of it mortgage driven, was around €200 billion.

The problem, of course, was the value placed on property at the time was unrealistic. By 2013, the value of housing wealth had dropped to less than €300 billion.

Now housing wealth, at €587 billion, is approaching the Celtic Tiger highs. With significant economic growth in the meantime and a rising population, economists in the ESRI have estimated that while house prices were overvalued in 2007, they are more in line with economic fundamentals now. This is not a perfect science. But with overall household debt now lower in cash terms than it was before the crash, household balance sheets are clearly in a much stronger and more resilient position.

2. Financial assets

Financial assets are made up of bank deposits and other financial assets. The value of these has risen from €404 billion as the pandemic hit to €491 billion now. So the gross value of financial assets now accounts for just over half of overall household wealth, compared to 42 per cent when the financial crisis hit in 2008.

Two things are of note here. One is the widely reported big rise in savings during the pandemic, The total amount held in deposit accounts by Irish households rose from €112 billion as the pandemic hit to €136 billion in October. There is always a significant amount in such accounts – it hovered around €100 billion since 2017 and rose a bit before the pandemic. But there are clearly excess savings built up now. There were signs as the economy reopened of the savings flow slowing, but this may now be reversed again – at least in part.

The second interesting issue is the rise in the value of listed shareholdings held by Irish households. This increased from €14 billion in late 2019 to €19.6 billion in the middle of this year. This is largely due to the swing in stockmarket value – the big drop in markets as the crisis hit reduced the value of shareholdings to €10.8 billion and it has since soared as share prices in most markets have risen strongly. The Iseq index of Irish shares is trading around 20 per cent up on pre-pandemic values. Households have also benefited from rising investment fund values.

Some of the rise may also reflect new investment in shares, but it is fair to assume that the bulk is due to the rising value of existing holdings. The huge pumping of cash into economies by central banks as part of pandemic supports has been good to those holdings assets, as it has sent a large flood of money looking for a home. The extent to which shares may be vulnerable as central banks start tapering support is a much debated question in markets and now an important issue for Irish household wealth.

3. Vulnerability

The Central Bank data also looks at household debt levels. This can give interesting insights – though obviously for a full picture we need also to look at the value of assets purchased with this debt, largely property. A theme since the last crash has been households paying down debt and being slow to take on new borrowings. Even though new borrowing has picked up in sectors such as mortgages, in recent years repayments have still outpaced new lending and overall debt has declined.

The difference from before the last crash is stark. Then, household debt stood at €200 billion and was 200 per cent of household disposable income. In the middle of this year borrowing was €127 billion, equal to around 100 per cent of national income. Household debt levels here have moved from the top of the EU league to around the middle, in line with EU averages.

4. Policy Implications

The figures suggest that household finances are on average a lot less vulnerable than before the 2008 crash and that measured wealth has risen during the pandemic. Much of this, tied up in property, is illiquid though economists believe a significant amount of the additional savings now in bank accounts will be spent as the economy reopens. How quickly this would happen is unclear – a fall in the level of new savings in the middle of this year shows that people are ready to spend. Trends in the pandemic will of course be crucial here.

While net wealth per capita has risen strongly, the Central Bank makes the point that different households have experienced varying fortunes during Covid-19. It is fair to assume that the wealth gap has widened. The better-off, property-owning, generally older population who have been more likely to be able to work from home have seen the value of their assets rise – the younger population, more likely to work in exposed sectors, did have much by way of assets in the first place.

Of course the divide isn’t into two clean groups – a surging job market, for example, will offer opportunities to many younger people too and wages are shooting higher in areas such as tech. But if the forecasts of rising house prices prove correct and rents stay high the wealth gap between those who own property and those who don’t will remain a big factor in the economy and politics.

The final issue is tax. Talks of a wealth tax are likely to remain in the debate. Political parties such as Sinn Féin who support this would say it should not hit the family home – indeed the party even opposes the local property tax. How best to tax wealth is a complex question. Property is still the bedrock of Irish wealth, but other assets are growing. Is it best to address this via some new tax, or changes to existing taxes like the local property tax or inheritance taxes, both hot button issues in Irish politics? Or is wealth fair game for more tax at all?