Cars, holidays and home improvements are driving demand for credit, as post Covid-19 spending habits pick up a gear. Latest figures from the Banking & Payments Federation Ireland (BPFI) show a surge in personal loans over the past year.

Despite a significant jump in interest rates over this period, personal loan drawdowns jumped by 25.2 per cent in the year to end-March 2023, up to €481 million. And the number of loans rose too, up by 27.8 per cent to 49,236. These figures represent new highs for personal lending.

A word of caution here, however; the data series began only in the first quarter of 2020, and in the era of Covid-19, personal lending was undoubtedly subdued. So, while record highs may have been reached, it started from a very low base.

The growth is also reflected in broader figures from the Central Bank, which show a 33 per cent hike in new consumer loans in the year to June 2023.

But what are people borrowing for? And if you’re in the market for a loan, what are the options available?

Car loans

The figures show that the move to electric cars has driven a surge in car loans, not only in the number of loans being taken out, but also in their value.

The number of car loans (15,167) taken out in the first quarter of 2023 was up by 27.4 per cent on the same period last year but the value of these loans was actually up by almost 40 per cent. Electric cars tend to be significantly more expensive than their petrol/diesel counterparts, so the move to electric is costing people more. And it may also be a reason behind the surge in lending – with people in the new car market more likely to buy electric cars. CSO data show that one-fifth of all new cars registered in the first seven months of the year were electric.

[ ‘Significant’ jump in value of car loan drawdowns amid rising pricesOpens in new window ]

As Brian Hayes, chief executive of the BPFI, notes, while the average loan value in the first three months of the year fell overall by about €200 to €9,763, the average car or auto finance loan rose by €1,073 to €11,678, “likely reflecting rising car prices and growth in electric and plug-in hybrid vehicles”.

According to Manuel Davila, managing director of Volkswagen Financial Services Ireland, one in five of all new car sales so far this year have been fully electric models.

Home improvement loans

Given the sharp rise in home heating and electricity costs that households have experienced over the past year, it’s no surprise that there has been a surge of almost 30 per cent in the number of home improvement loans being taken out with the banks.

Lenders are cashing in on this demand, with many offering their most favourable rates to those looking to carry out such improvements.

Holidays, weddings and other

With a return to the sun for a break on the minds of many, and weddings increasingly becoming two- and three-day events – often in those aforementioned sunny spots – there has also been an increase in people borrowing for these events.

Figures from the BPFI show that the number of loans for holidays, special occasions such as weddings, as well as education, rose by 27.4 per cent to 20,119 in the first quarter of this year. People aren’t necessarily borrowing more, however, as the value of such loans increased by only 18 per cent in the period to €146 million.

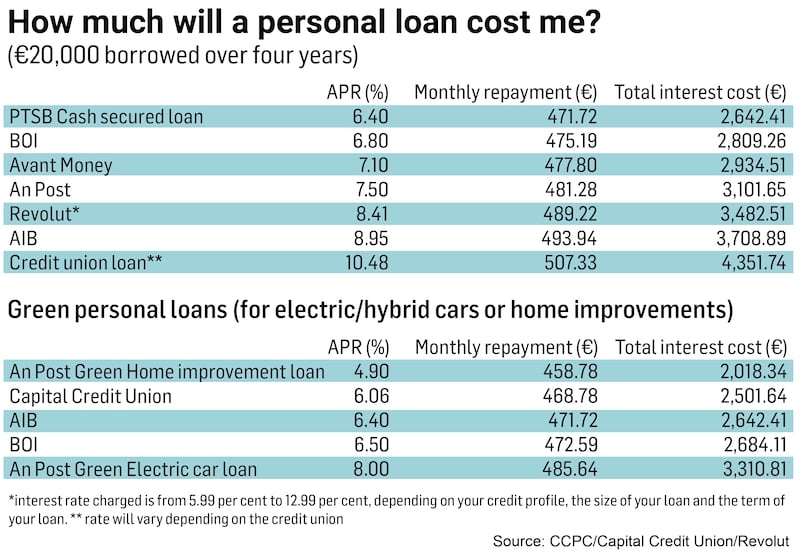

Shop around

As our table shows, it does pay to shop around if you’re in the market for a personal loan. Somewhat surprisingly, perhaps, despite sharp increases in European interest rates over the past year, personal loan rates haven’t risen accordingly – or at least not yet. Central Bank figures show that in the year to June 2023, the interest rate charged on new consumer loans rose by less than half a percentage point to 8.19 per cent.

Daragh Cassidy, head of communications with comparison site Bonkers.ie, confirms personal loan rates haven’t jumped hugely over the past year. While both An Post and Avant Money increased some of their loan rates by just over one percentage point back in February, some of their rates actually fell, Cassidy says, while among the main lenders there has been little upward movement.

Nonetheless, it still pays to shop around. Personal loans are typically for amounts from a couple of thousand euro up to about €70,000 or so. For anything in excess of this (and sometimes for amounts less), it can make sense to look at a mortgage-type arrangement if you do own a property, such as releasing equity etc, as this can be a more cost-efficient option.

Remember, if you keep the term as tight as possible, you will save money. For example, €20,000 borrowed over five years will cost you €3,143.60 in interest over that period – but just €1,871.19 over three years, based on an APR of 6.06 per cent.

One of the lowest rates available is the 6.4 per cent available from Permanent TSB (PTSB). Opting for this over a credit union loan at about 10.5 per cent will save you as much as €1,700 over the life of a four-year loan.

However, be aware that such a low rate does come with restrictions. As a cash-secured loan, the APR of 6.4 per cent is based on you offering cash security of 100 per cent for the loan. What this means in practice is that you will need to have a similar amount saved in another account. So, if you’re borrowing €20,000, the bank will take a “lien” on a deposit account where you have €20,000 saved. This lien means that you can’t withdraw money from the account and, if you do not or cannot repay the loan, the bank will be entitled to access the money in the deposit account to pay it off.

[ How to retrofit your home and slash your energy billsOpens in new window ]

If you can offer cash security of only 75 per cent (ie savings of €15,000 for a €20,000 loan), the APR rises to 7 per cent, or 8 per cent where security of just 25 per cent (ie savings of €5,000) is offered. Given such level of security, it could be argued that the rate on offer should be even cheaper.

For amounts of €20,000-€65,000, Bank of Ireland’s 6.8 per cent APR may be an alternative, as you don’t have to offer cash security.

Similarly, Revolut offers loans of €2,000-€30,000 at what it says are “market leading” rates starting at just 5.99 per cent. If you can get that rate, then it is market leading – but, as the lender itself says, rates on offer vary from 5.99 per cent APR to 12.99 per cent APR – at which point it would be pitching itself as the most expensive available. What rate you are offered will depend, the lender says, on your credit profile, the size of your loan and the term of your loan.

Go green

If you’re in the market for a new electric/hybrid car or for some home improvements aimed at boosting the energy efficiency of your home, a green loan may be an attractive option, and the cheapest.

An Post has a rate of just 4.9 per cent if you’re looking for money to upgrade your home. This means that borrowing €20,000 will cost just €2,021.25 over four years, compared with €3,101.65 if you opt for a typical personal loan with the lender. But it may be tricky to qualify for the loan, as An Post says that a minimum of 50 per cent of the loan value must be availing of grant support by Sustainable Energy Authority of Ireland (SEAI). Depending on the scale of your project, this may not be possible.

Other options include your local credit union. Capital Credit Union, for example, has a rate of 6.06 per cent for such loans, while both AIB and Bank of Ireland offer slightly higher rates of 6.4 per cent and 6.5 per cent, respectively.

If you’re looking for forecourt finance for a new electric car, there are still deals to be had. Despite interest rate hikes, it is still possible to get APR deals of as low as zero per cent on some models, says VW’s Davila.