A lack of evidence of a bubble in house prices has been described as “somewhat reassuring” by the Economic and Social Research Institute.

The think-tank’s new report examining the State’s housing market says the “expected robust performance of the Irish economy” between now and 2020 “is likely to result in continued upward pressure on prices”.

Anticipated house price inflation of 20 per cent over the period could add more than €50,000 to the cost of an average three-bedroom semi-detached house, although the impact will depend on the location.

A recent survey by the Institute of Professional Auctioneers and Valuers pointed to huge price discrepancies across the State, with the average price of a three-bedroom semi-detached home in Dublin 4 put at €975,000 compared with just €90,000 in Longford.

The ESRI report uses “well-established” models including economic fundamentals such as employment and supply as well as cross-country comparisons of relative housing affordability and standard house price-to-rent ratios to make its predictions.

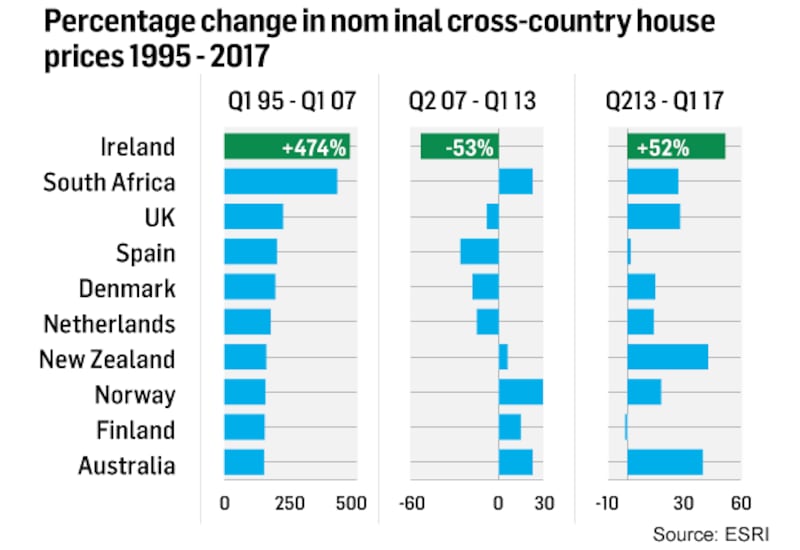

The report shows that from 1995 to 2007 house prices in the State climbed 474 per cent. By contrast prices in the UK climbed 222 per cent, while house price inflation in Spain was 199 per cent. Most other countries in the EU saw prices increase by 100-200 per cent over the period.

Between 2007 and 2013, and in the wake of the international banking crisis, property prices here fell 53 per cent before climbing 52 per cent in the post-crash period.

Prices in the UK fell 8 per cent up to 2013 and then climbed 28 per cent, while in Spain prices fell 26 per cent after the crash and climbed 2 per cent since 2013.

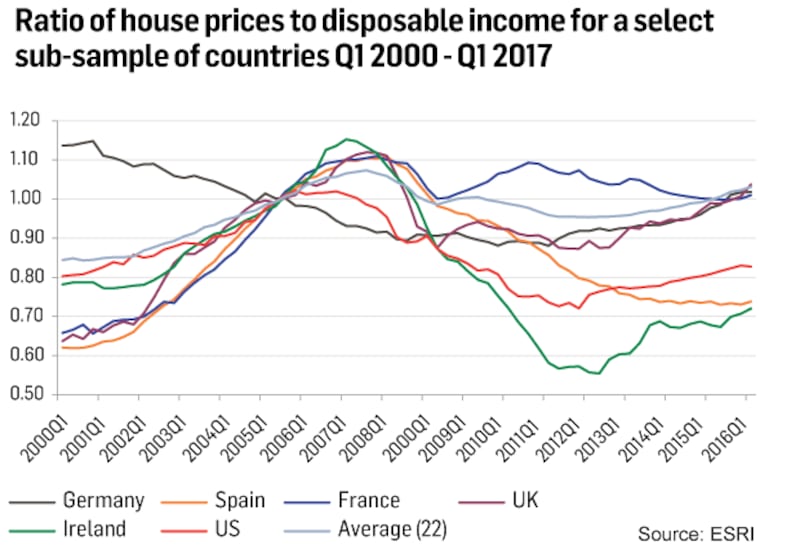

The ESRI finds that when all the peaks and troughs are examined and compared with actual Irish disposable income and a cross-country average of the relationship between disposable income and house prices, prices here over the period 2000-2017 “experienced overvaluation in the 2006/2007 period and significant undervaluation in the post-2008 timeframe”.

It also says that when compared with international averages, house prices are more affordable here than in many developed countries in the OECD.

The rental ratio

The report says house price-to-rent ratios have remained static since 2012 and that while rents are rising significantly, reflecting the strong underlying performance of the economy, the fact that the ratio is both relatively stable suggests “that no bubble or overvaluation is apparent in the Irish property market at present”.

It points out that price increases since 2013 have occurred in the absence of any significant increases in mortgage credit.

“One issue which will require ongoing, critical assessment is likely future developments in the provision of credit,” the report says.

“Much of the persistent increases in house prices observed since 2013 have occurred in the absence of any credit growth ... Consequently, as the Irish banking sector slowly heals itself and economic growth continues, credit conditions are likely to become more expansive over the medium term.”

It warns about the danger that, similar to the 2003-2007 period, "credit growth itself will fuel greater house price inflation. In that regard the new macroprudential policy framework adopted by the Irish Central Bank will be hugely important."