So far in 2022 financial markets are hanging in. But with inflation soaring, the interest rate cycle turning and continued uncertainty about Covid-19, investors now face significant uncertainties. The return of inflation, particularly if higher rates persist, is very important. So far markets are counting on a a benign outcome – strongish growth and some inflation, but not too much.But the dangers are obvious. 2022 looks like a year of living dangerously for investors.

1. The Omicron Trade

Equity markets had a few sharply negative days towards the end of last year, as news of the emergence of Omicron rattled nerves. But they are now generally on the rise again. This is driven by two things. One is the evidence that much of the world economy can continue to operate, even during a Covid wave. Markets crashed when the pandemic broke, but central banks stepped in on a major rescue mission and then, as time went on, confidence returned in many sectors.

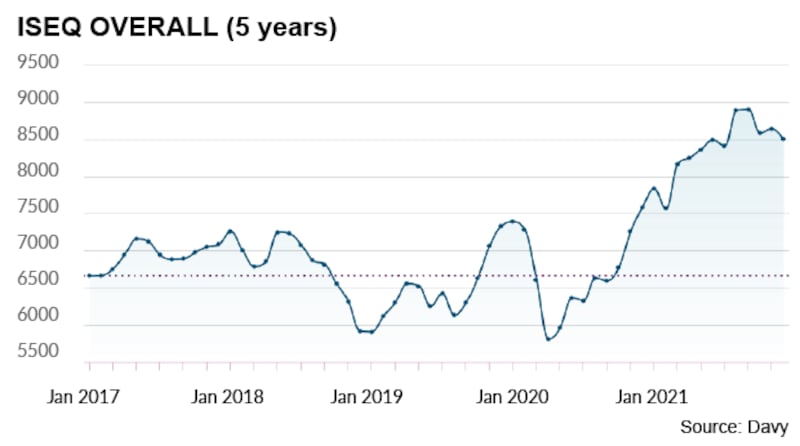

Some exposed stocks have suffered – look at cruise line stocks, for example – and others have languished. But stockmarkets in general have prospered, driven by the massive money printing of central banks – which has left cash looking for a home – and the resilience of sectors such as big tech. The tech-dominated Nasdaq index is 60 per cent above its pre-Covid level. Of course this has been driven by the strong performance of a few big players, some of which have benefited from trends such as working from home. But generally it has been a strong period for equity markets, with the Iseq index not far off 20 per cent up on its pre-Covid level.

In the optimistic scenario which is now underpinning a lot of market trading, the Omicron wave will pass and with it the era of restrictions, allowing economies to return to some kind of “ normality”. How realistic this is we simply don’t know. And, as we will consider below, the rise in inflation is putting pressure on central banks to withdraw support from markets and leading to a change in trading patterns.

Like us all, market traders will closely watch Covid trends. But equity markets look vulnerable to bad news, or to any general slowdown in growth rates going through this year. Looking at European markets, analysts at Bank of America see risks from slower growth, hawkish central banks and highly valued markets, with stocks that swing with the economic cycle particularly at risk. Markets are vulnerable as they are not currently not factoring in significant risk premiums, it warns. This analysis is a minority one, but it shows the dangers.

2. The inflation risk

Inflation is back, With a bang. The US inflation rate is now a whopping 7 per cent, a fact shrugged off in the immediate market reaction as the figures were no worse than anticipated and Fed chairman Jerome Powell has said the rate will fall and the Fed can handle it. Soaring energy prices are part of the reason – and most analysts expect these to ease a bit in 2022, though events in the Ukraine remain a threat. But the inflationary spike has gone on longer than central banks had hoped for and is peaking at a higher level. And so the Bank of England has increased its interest rate, the Fed is expecting three rises in 2022 (bringing its key rate to around 1 per cent) and all central banks, including the ECB, are going to withdraw support from bond markets, which will send long-term interest rates higher.

The return of inflation is a key issue for markets. First, it influences the real – after inflation – return on assets and thus fundamentally alters the mindset of investors. Second, it puts pressure on central banks to change policy and move more quickly on interest rates. And third, and linked to the second point, it leads to an increase in bond interest rates – or long-term interest rates – which are a key marker for financial markets.

If the cycle continues as many expect – or hope – inflation will ease a bit and central bank rates will rise a touch, but not enough to choke off growth. In this relatively benign scenario cash would be likely to move from riskier stocks not yet generating cash returns to more defensive, higher yielding ones. “ Spec tech” , as it is dubbed – technology companies not yet generating a dividend return for investors – are relatively less attractive as interest rates rise, making safer homes for cash relatively more enticing. But overall equity markets would continue to rise in this benign scenario. It does of course seem to require most things to go “right.”

If the inflation rate stays high and central banks are under pressure to tighten policy more quickly, valuations could come under pressure. And bond markets could take fright, feeding back into wider market nervousness.

Equity markets famously took fright in the so-called "taper tantrum" of 2013, after Ben Bernanke, then Fed chief, signalled an unwinding of supports introduced during the financial crisis. But while the equity drop was short-lived, bond markets took a longer hit, with 10-year US rates rising as high as 3 per cent, a big jump, though still low by historical standards. Higher US interest rates and a stronger dollar can also knock on to unease in emerging markets. And if inflation becomes embedded it can damage confidence, spending and investment.

3. A new era?

The key issue for investors is whether the return of inflation is temporary or will be longer-lasting. A temporary rise in inflation increases the price level and hits returns for a period, but a sustained rise presents new challenges in trying to get real (inflation-adjusted) returns on investments over the longer term. It fundamentally alters mindsets. Since the 1980s there has been a general downward drift in inflationary pressures and thus interest rate cycles have topped out at lower levels. Part of this is also attributed to ageing populations – and thus the need for less incentive to save as older households so so anyway. As well as nominal interest rates, real interest rates have also been on a long-term decline.

The return of a 7 per cent US inflation rate – and a rate of close to 6 per cent in Ireland – is taking us back to the early 1980s. Many younger people have simply never experienced this.

Whether those saying this is transitory are correct, or not, is thus a vital question, with massive implications for investors, savers and borrowers over the next few years and for economies generally. Some of the factors which have pushed up prices may well ease – a decline in energy prices is expected and global supply lines are anticipated to ease, though China’s clampdown in response to Omicron could delay this. But there will be nervousness in central bank boardrooms come springtime if inflationary pressures are not by then sharply on the decline.

Investors have had to take risks to get a return in recent years. But equities have done well – up not far off 7 per cent globally last year – and bond markets have mostly held the gains of recent years. With low inflation, the massive money-printing exercise by world central banks has helped to generate a significant return for investors and held down risk. But a return of inflation and a running down of central bank supports means things are looking a lot more complicated and risky for 2022.