Irish wage growth is storming ahead. By any standards – historical, relative to the rest of Europe or compared to the general rise in prices – wage growth of 4.1 per cent in the last year is a good result. The rapid rise in jobs seen since 2013 has translated, over the past few years in particular, into higher wages. Weekly earnings have risen by close to 10 per cent over the past five years, a period during which there has been almost no generalised rise in prices. With total employment rising by more than 300,000 over the same period, the bounceback from the trauma of the crisis has been remarkable.

There are significant differences from sector to sector, looking either at the last year or the long-term trend over the past decade. Most sectors have risen over the past few years, but for some this follows sharp falls during the crisis. Others never took much of a hit – but are now rising strongly. The bottom line is that if you want to make money, work in tech.

It is sometimes easy to forget what economics is about. But the bottom line is improving people’s standards of living. And the Irish jobs market has delivered - in spades – in recent years. As the market has got tighter and as the Government could again afford to increase public sector earnings, pay growth has accelerated.

What is the outlook ? Recent data do suggest a slowdown in hiring in the fourth quarter, and recruiting sources suggest many companies are now distracted by Brexit and some have put investment plans on hold. If a no-deal Brexit can be avoided, then companies will go back to planning their expansions and worrying about getting new staff and holding on to the ones they have.

If there’s a no-deal Brexit, then all bets are off, with a recent forecast from Ulster Bank suggesting losses from a no-deal in exposed sectors like food and the knock-on from this – a cost of 45,000 jobs – could completely offset gains elsewhere in the economy this year. In turn this would sharply slow pay growth.

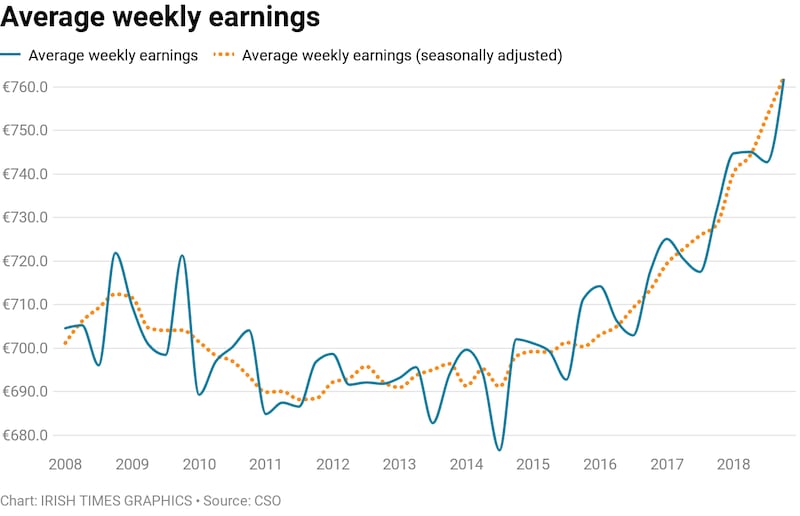

1. What are the key pay trends?

Average weekly earnings were €761.65 in the fourth quarter of last year, according to the data just published, an increase of 4.1 per cent from one year earlier. Average hourly earnings were up 3.8 per cent – so the weekly total also involved a small element of additional hours, where the average rose from 32.4 per week to 32.5. Wage growth here is ahead of the EU average, which was running at 2.7 per cent year on year in the third quarter of last year.

In the last five years, weekly earnings here have risen by 9.7 per cent, though there are huge variations from sector to sector, which we will look at below. Research by the European Trade Union Confederation on real wage growth – pay increases adjusted for inflation – puts the performance here in a reasonably favourable light compared to elsewhere in the EU.

Looking at 2017 alone, it found six countries where real wages fell – in other words inflation ran ahead of wages. These included Spain, Italy, Belgium and the UK. In a further 10 countries, real wage growth was 0 to 1 per cent. In 12 other countries real wage growth was higher, with Ireland estimated to be 2.3 per cent. Most of the other higher-wage-growth countries were in central and eastern Europe.With inflation here at 0.7 per cent last year, the 4.1 per cent earnings growth equates to a 3.4 per cent real increase.

Over the longer term, the ETUC found that, notably, nine countries had lower real pay levels in 2017, compared to 2010, including Portugal, Spain, Italy, the UK and Belgium. In Ireland the gains were put at 6 per cent in real terms over the period – and adding 2018 would now be over 9 per cent.

So gross pay packets – in real terms – are now back over pre-crash levels. However, for most employees a higher tax burden on income will have eaten significantly into the gains.

2 . Who is winning and who is losing out ?

Average weekly earnings increased in all 13 sectors of the economy over the past year. The most rapid rise was a 10.5 per cent increase in a sector called administration and support services, which includes a wide range of jobs including people working in HR, security, office admin, call centres, travel agents and the recruitment industry.

The other big winner over the past year has been the transport and storage sector, where average earnings are up 9.1 per cent. This sector includes employees working in all sectors of transport as well as warehousing and the courier industry.

More modest increases were recorded in the wholesale and retail sector (plus 2.3 per cent ) and accommodation and food services (plus 4 per cent).

There are very significant differences between average earnings in different sectors. At the top stands the information and communications technology (ICT) sector, dominated by multinationals, where average earnings are €1,175 (or over €61,000 per annum), followed by finance, insurance and real estate at €1,085.

The lowest average weekly earnings were €360.73 in accommodation and food services and €493 in the arts, entertainment and recreation and other services. As well as people employed in the arts, this latter sector also includes the sports industry, bookies, libraries, museums and those working in repairs of phones, computers, electrical appliances and so on.

There is a twist in the higher earning category, however. Although the ICT sector has the highest take-home pay, the highest pay per hour is in education at €36.27, compared to the national average of €23.46. Average weekly paid hours in education are 23.7 versus a national average of 32.5.

The other key trend is the long-term one, where there is massive variation between sectors. Some lost heavily during the crisis and are bouncing back. Others never lost much in the first place and are thus now way ahead of pre-crisis levels. At one extreme we have construction, which had a catastrophic fall in employment from 147,000 in early 2008 to a low of 52,300 by 2013. Pay collapsed quickly, dropping by 14 per cent by the end of 2011. Over the past few quarters it has finally climbed back above its pre-crisis peak, with average weekly earnings of €810.60, around 2.7 per cent over their 2008 level. This would not be enough, however, to offset higher taxes for many workers in the sector.

The low-paid accommodation and food services sector suffered a pay fall of almost 12 per and has now recovered to around 3 per cent above its 2008 level.

In other sectors the trend is different. Despite the fallout in the financial sector, pay levels did not fall significantly and in the fourth quarter of last year were 11 per cent ahead of a decade earlier, at €1,143 per week.

However, even more significant gains were made elsewhere. Earnings in the highest-earning ICT sector never fell back much during the crisis and are now 22 per cent up over the past decade. Earnings in professional, scientific and technical services are 14 per cent ahead. And in the admin and support sector earnings are also up almost 22 per cent, having not fallen too much during the crash and risen strongly in the recovery. However, in gross terms average pay here remains modest at just over €600 a week.

In bigger sectors, gross weekly pay in manufacturing is now 11 per cent ahead of 2008 levels ( at €877 per week) and in wholesale is up 15 per cent ( at €596). In public administration – covering the civil service – weekly pay in the fourth quarter of 2018 is 2.7 per cent down on a decade earlier.

3. What are the key issues ?

The share that employees are getting of the fruits of economic recovery are a major issue across the industrialised world. Here, at least in some sectors, the fight to attract employees, from Ireland and abroad, has led to a sharp rise in earnings in the last couple of years.

However, the gross pay levels show the market remains divided between the generally higher-paying multinational-dominated sectors – particularly ICT and science and the domestic economy. Pay in domestic services – retail and accommodation and food services, while rising, remains low.

A recent report from think tank Tasc argued lower-paid employers in Ireland – not the very poorest 10 per cent in society but the groups just above them – receive a lower share of income than in the more equal EU countries, creating a squeezed lower middle. Certainly high prices and high housing costs would be an issue for many in this group.

For more middle- to higher-income earners, the picture is mixed. Some in higher-paid sectors will have seen significant real income increases in gross terms and large enough longer-term rises, even when the higher post-crash tax burden is counted in. The squeeze here will come on those who have more recently entered the housing or particularly the rental market, where prices are well in excess of Celtic Tiger peaks. But for others real earning power is now rising sharply.

While the jobs market has been delivering in recent years, the gains have been spread unevenly. A few more years of pay growth at 2018 levels would make a significant difference. The key question now is where jobs and pay growth is going from here.

Economists argue that despite the low unemployment rate, the actual proportion of people in work in Ireland suggests sufficient wages will still attract people to return to work. So more supply will come – if the demand is there. Immigration has also traditionally filled gaps, though the price of housing is a constraint here.

However, the big immediate shadow is the risk of a no-deal Brexit. It is hard to overstate the threat this poses to the domestic economy and to rural Ireland. If a no-deal were to happen, it would hit numbers and pay hard in some sectors, with a knock-on impact across the economy. If it is avoided, and we enter a transition period where not much changes for a couple of years, then slower world economic growth will be a constraint, as will rising costs for employers, but pay and jobs growth should continue.

The Central Bank has said pay could rise by another 3.5 per cent or so on average this year and next. That, added to 2018 gains, would be significant. But it is now all depending, of course, on Brexit.