If you tried to create a more difficult backdrop against which the European Central Bank (ECB) is increasing interest rates, you could hardly find one. Until recently there was the war, soaring inflation and the threat of a euro-zone slowdown or even recession, particularly if Russian gas supplies are cut over the winter. Now — to really make it Mission Impossible — the Italian government has collapsed, increasing the risk of market pressures in response to the ECB’s policy moves. And in a supreme irony, the man at the centre of the Italian drama — Mario Draghi — stood up as ECB president almost exactly 10 years ago with his famous intervention that the ECB would do “whatever it takes” to save the euro. Then, the ECB faced a potential slump into deflation — now the problem is runaway inflation and the ability of the central bank to rein in price pressures in the face of a rapidly slowing economy.

In the circumstances, there was no “right” decision from the ECB. The decision to push up interest rates by a full half of a percentage point — contradicting earlier statements that a quarter-point rise was planned — was a response to soaring inflation, now at 8.6 per cent across the euro zone. To protect against this leading to speculation against more vulnerable countries, notably Italy, the ECB also announced a new programme to allow it to intervene in markets — subject to terms and conditions.

The two parts of the decision appeared to be a trade-off between the different factions of a divided governing council — agreeing to a full half-point rise meant the more hawkish northern Europeans got on board for the new mechanism to support countries under pressure, the so-called Transmission Protection Instrument (TPI).

[ Explainer: Why is ECB raising rates now for first time in more than a decade?Opens in new window ]

[ ECB’s first rate hike in 11 years to hit €25bn of tracker loansOpens in new window ]

Both legs of this policy look wobbly enough. Higher interest rates from central banks cannot attack the primary cause of inflation — higher prices for energy and other commodities. They may help to stop inflation getting embedded by taking money out of the economy, but this will only accelerate the economic slowdown already under way. And the new promise to help countries under attack on the markets by buying their bonds comes, as expected, with terms and conditions on budget policy attached. This will be controversial, particularly in Italy, and possibly impractical given that the country is heading for a general election. The markets may well decide to test the ECB’s resolve here, sooner rather than later.

RM Block

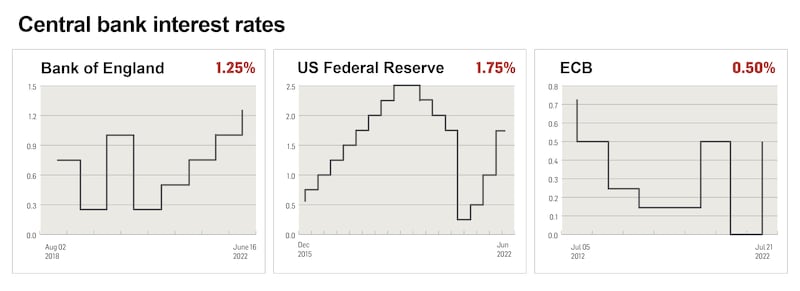

Nonetheless, it was a landmark day for the ECB. Interest rates are being increased for the first time in 11 years — and the clear message is that there is more to come. Using typical central bank speak, ECB president Christine Lagarde told a press conference following Thursday’s meeting that at future ECB meetings “further normalisation of ECB interest rates will be appropriate”. The risk for borrowers now is that there will be a rapid move upwards in interest rates over the autumn, perhaps two or three more interest rate moves, taking the ECB base rate — its refinancing rate — which is 0.5 per cent after Thursday’s move, up to 1.25 or even 1.5 per cent by the end of the year. For now, another increase in September looks very likely, but with the euro-zone economy slowing, what happens beyond that is uncertain.

Lagarde left the ECB’s options open for the September meeting in terms of the scale of the increase — it will depend on inflation data — but continually repeated that interest rates were now on a normalisation — increasing — path. It looks like there will be no more flagging of when interest rates will rise — having had to change tack at the last minute this time, with late leaks probably designed to prepare the way, Lagarde referred to moving to a “meeting-by-meeting approach”.

No more than the rest of us, the ECB does not know what will happen next. Its baseline is that the euro zone will avoid recession this year and next, though the risks are acknowledged.

“I think the half-point increase move may be a case of trying to get rates up now while they still can,” said Megan Greene, a senior fellow at the Harvard Kennedy Business School and global chief economist at the Kroll Institute. “If Russia wants to cause havoc for Europe by turning off or down the gas taps, it is incentivised to do it sooner than later, before Europe reduces its dependence on Russia for gas.”

In turn this could hit economic growth and make it harder for the ECB to hike rates further.

There are already, Lagarde said, signs of a slowdown in growth across the euro zone. If lower demand — and perhaps some easing in energy prices — takes pressure off inflation, then interest rates would increase more slowly. The central bankers’ nightmare is that growth falls but inflation stays high — so-called stagflation — putting pressure on the ECB to keep increasing interest rates in the face of slumping economic growth. Nobody knows how the balance might be struck, but the ECB’s mandate focuses only on keeping inflation around 2 per cent — a point also underlined by Lagarde at Thursday’s press conference. The ECB is walking a delicate path between controlling inflation and not pushing the euro-zone economy into recession, and as of now no one knows whether achieving both is even possible.

The impact on many Irish consumers will be fast. Tracker mortgage rates — about 250,000 hold these mortgages — will increase immediately by half a percentage point and we will watch to see what banks do with variable interest rates; they too will rise sooner rather than later. Those on fixed interest rates, including the vast bulk of newer borrowers, will be protected for the length of their fixed-rate term, though they will face higher rates when this term ends. This is key for many newer borrowers. The cost of fixed-rate loan offers for new borrowers will increase. The long period of super-low interest rates is coming to an end. What we don’t know is how high interest rates will now rise.

The clear indication from the ECB is that interest rates are going to march higher now later this year and heading into 2023, but the markets still have to be convinced that it can pull this off. While borrowers will rue the end of an era of very low interest rates, just how far interest rates will now rise remains very uncertain. But rise further they will, initially at least, particularly as the ECB is already well behind other major central banks such as the US Fed and the Bank of England in terms of hiking rates.

“Irish mortgage rates are already among the highest in the euro zone, so there is room for the banks to absorb some of the increases, at least initially ” said Daragh Cassidy of Bonkers.ie.

“However, the US, UK, Canadian and New Zealand central banks have all raised rates by well over one point over the past few months. If the ECB feels under pressure to follow suit it’ll put another big strain on households’ finances at a time when they can least afford it.”

The indications on Thursday were that it wants to do so, but it is not clear whether it will be able to.

“The ECB is trying to catch up by front-loading a return to ‘normal’ interest rates,” said Dermot O’Leary, chief economist at Goodbody. “We don’t know exactly what normal is, but it may eventually be ECB rates close to 2 per cent. Lagarde has signalled that she wants to make progress quickly, which points to another 0.5 point increase at the September meeting.”

Beyond that the markets are betting on further increases later this year as the ECB closes the gap with other central banks, but these expectations can quickly change.

The other factor which may well affect the path of ECB interest rates is whether tensions appear in the euro zone. The ECB has been basically underwriting the borrowing of European Union governments during the pandemic by buying their bonds on the market. Now this support is being withdrawn and the markets have reacted by widening the interest rate gap between Germany and what are perceived as less financially strong member states. Italy, with its high debt and uncertain growth outlook, is in the firing line, with its 10-year interest rate now over 3.5 per cent, now more than 2.2 percentage points above Germany.

To combat this, the ECB has announced the new TPI which would allow it to intervene in government bond markets where it feels unwarranted increases in borrowing costs are happening. The ostensible reason is that these increases can mean its monetary policy is not being reflected consistently across the euro zone. This new mechanism can be triggered by the ECB council, but is subject to terms and conditions, including member states abiding by EU budget rules, now in abeyance, pursuing sound policies and meeting the rules of the EU recovery fund, set up during the pandemic to help boost investment, particularly in southern Europe.

With the Draghi government having fallen, it is uncertain whether Italy will meet the conditions for disbursement of the next round of recovery funding. If not, Italy may not qualify for additional help. The ECB council would also have to judge that the increase in Italian borrowing costs was unwarranted — in other words, not justified by the conditions of the Italian economy. “[I]nterest rate spreads should exist in the euro zone to reflect underlying differences in fiscal approaches and risk across the currency area,”, noted Greene. How exactly decisions will be made in practice on the TPI — and what other scope the ECB has to support countries under pressure as it reinvests proceeds of its pandemic programme — are now vital questions. And as the TPI was clearly a compromise deal at the ECB council, investors will judge the ECB by what it does, rather than what it says. Some key issues, such as how much of a country’s debt it can hold via all programmes, also remain unclear.

“Clearly there is now a tool there to target spreads but using it will be still technically difficult and possibly subject to legal challenge,” according to O’Leary of Goodbody.

Previous programmes have been challenged — generally unsuccessfully — in German courts.

Borrowers thus face into a new era. So too do savers, though flush with deposits Irish banks may be slow to increase savings rates. In time, however, they too will rise. The world of rock-bottom rates is behind us.