I live in a semi-detached house that was built in the 1970s. The heavy rain of recent months has resulted in the accumulation of water in the sub-floor void. I am concerned the accumulating water will lead to rising damp and I want to know how the water is getting in and how to stop it. I am not sure where to begin.

The floor is comprised of timber with joists. There is about 1ft of sub-floor space, and I'm almost certain there's a concrete oversite. I reckon the sub-floor oversite is about 5 inches (127mm) lower than ground level.

Any advice on where I should begin would be greatly appreciated.

The floor construction you mention is called a suspended timber ground floor. The floor consists of a series of timber joists arranged parallel to each other, supported at each end on small sleeper walls, as well as at intervals along their length with honeycomb sleeper walls and wall plates (wall plates are long, horizontal timbers resting on the honeycomb wall supporting the parallel joists).

The honeycomb walls are constructed in such a way as to allow a continuous passage of air to flow beneath the suspended joists. To give access to this air, air bricks are also built into the outer structural walls of the building. This constant flow of air is necessary to keep the timber dry and prevent the possibility of dry or wet rot occurring.

Incorporated into the construction of the sleeper and honeycomb walls is a damp-proof course (DPC) which acts as a physical barrier to prevent dampness rising up through the blockwork to the timber floor. DPC is normally inserted below the floor wall plate about 220mm above the “concrete oversite” (the concrete fill below the floor) and so rising damp is unlikely to occur within the honeycomb walls. A DPC should also be included within the perimeter walls of the property above external ground level at a minimum of 150mm “splash-back height”.

In your case, if the external floor level is constructed 127mm above the internal level, there is a possibility of water breaching the DPC resulting in rising damp to the external wall and potentially seepage through the perimeter wall (subject to construction) which would, as you suggest, accumulate in the sub floor void.

The principle behind ground-floor construction is that the internal sub-floor level is higher than the external ground level to limit the possibility of water seepage.

You should also explore the potential for other water sources, ie to ensure there is no leaking pipework or blocked gully traps that may be attributable to water within the void.

I would recommend that the floor void is monitored over a period of four months to determine if the water within the void will evaporate.

Subject to monitoring it may be necessary to reduce the ground level around the building in line with the sub-floor “concrete oversite” .

Andrew Ramsey is a Chartered Building Surveyor and Chartered Project Management Surveyor and is chairperson of the Building Surveying Professional Group of the Society of Chartered Surveyors Ireland (SCSI)

Calculating CGT

I notice CGT has cropped up over the past few weeks. Can you clarify the methods used to calculate this, assuming a house bought in 1985 for about €40,000, which was my principal private residence until 2000 and was renovated at a cost of €20,000 – new kitchen, bathroom etc – thereafter rented and sold in 2015 for €250,000? The renovation costs were not used as "capital expenditure" for annual returns.

I have two queries: as the renovation costs have not been used, am I right to assume they factor into the CGT when disposed? And is indexation used to bring the original purchase price and renovation costs up to today’s values?

Also, in a recent example there was no mention of the original purchase price and if this was adjusted and how. Can you clarify if the original purchase price should be indexed to today's value using a sliding scale provided by Revenue?

For significant renovation costs, are these not factored into the calculation, (ie selling price less indexed purchase price less indexed renovation costs etc = gain; therefore CGT = gain at 33 per cent). A considerable amount so hopefully I'm wrong.

Relief is given for a gain on the disposal of a dwelling house (or part of a dwelling house) which is a person’s only or main private residence. Where the house has not been occupied as the owner’s principal private residence throughout the whole period of ownership (apart from the last 12 months) a fraction of the gain is taxable.

Where only part of the dwelling house qualifies, the gain is apportioned. There is also apportionment to ensure that the relief is restricted to the proportion of the period of ownership during which the dwelling house was the only or main private residence and for this purpose the dwelling house is treated as having been so occupied during certain periods of non-residence. One acre of land which is used as a garden or grounds of the residence is also exempt.

A deduction is allowed for enhancement expenditure such as on renovations that will increase the cost of the house. These costs should not have been previously deducted for income tax purposes.

There is also tax relief for inflation up to the end of 2002 for any disposals made on or after January 1st, 2003. It is called indexation relief and is shown in the example below.

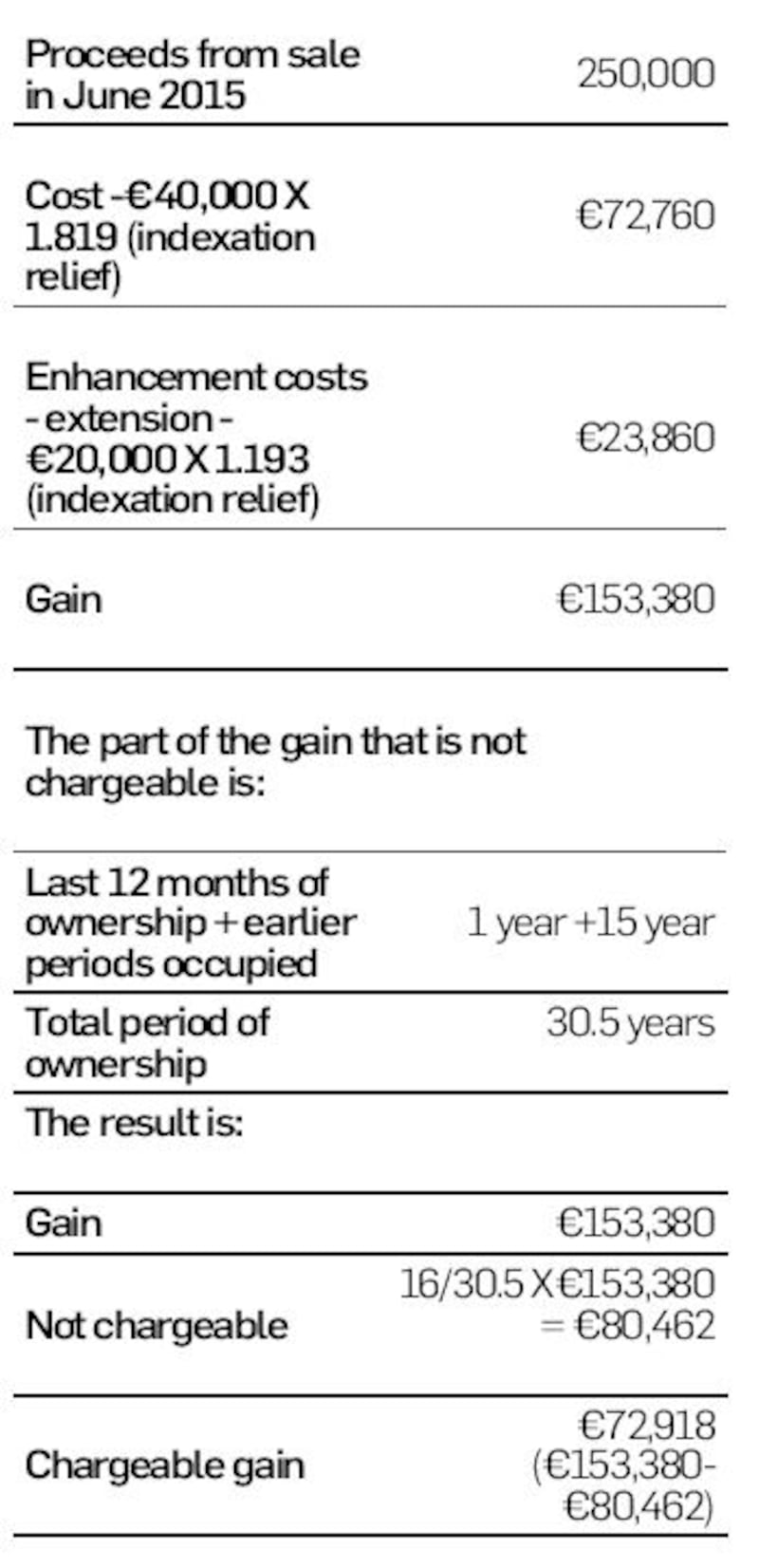

Example (assuming all the relevant information is below):

An individual buys a house for €40,000 (including expenses) on January 1st, 1985 and moves in immediately to occupy it as their principle private residence.

The person spent €20,000 on an extension in January 2000. The person moved out of the house at this time, into rented accommodation.

The house is let until it is sold for €250,000 on June 30th, 2015. The gain is calculated as seen in table.

Gareth Murphy is a tax senior with Baker Tilly Ryan Glennon