Interest rates are at historic lows in Europe and savers are feeling the pinch. But, chastened by their experiences over the past few years, Irish savers and investors are still holding fast to their deposits, reluctant to chase a better – if riskier – return by giving up the protection a deposit account offers their capital.

Central Bank figures for example, show in the 10 months to October 2014, deposits held by Irish households grew by more than 1 per cent to €92.2 billion. While the economic crisis may have abated, deposits have only fallen by 7 per cent since the peak of €99.4 billion in early 2010.

"It's the idea of "penultimate preparedness" – the idea of preparing for the event that's just happened, so a lot of people are invested like the financial crisis is about to happen again," says Ian Quigley, director of investment strategy at Investec Wealth & Investment Ireland.

Espoused by Fidelity investor Peter Lynch, "penultimate preparedness" is a way for people to make up for the fact that they "didn't see the last thing coming along in the first place".

But staying overweight in cash may be a risk in itself.

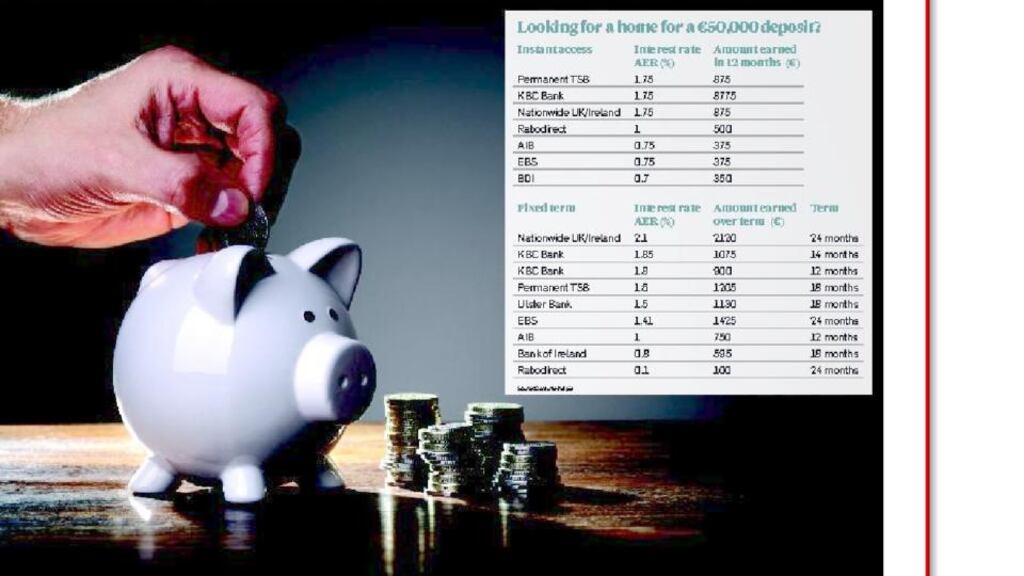

Deposit rates

Irish people’s predilection for deposits comes against a background of a downward push on interest rates, although the evidence suggests that savers are not necessarily aware of how their money is performing.

Indeed a recent survey from Zurich Life found that many Irish people thought they were earning over 3 per cent on their deposits – even though in many instances it was less than 0.5 per cent.

Back in 2010, a saver could have expected to earn upwards of 4 per cent on a lump-sum deposit. Now rates are at best languishing at around 2 per cent – and at worst are continuing to fall. This month for example, Bank of Ireland cut the rates it offers savers, decreasing its regular saver account from 1.5 per cent to 1.25 per cent, and the rate it offers for its 30-day notice account from 0.7 per cent to 0.4 per cent. And it's not the only one.

Permanent TSB has just cut its rates too, slashing 0.5 per cent off its "safari saver account", to bring it down to 1.5 per cent, and 40 basis points off its regular savings account, to cut it from 2.5 per cent to 2.1 per cent. While better rates are available – Nationwide UK's rate of 2.1 per cent over 24 months is one of the better offers on the market for example – overall deposit rates are far off the artificial highs of the past few years.

On top of that, savers may have to hand back up to 45 per cent on any return they make to the government, given the Dirt rate of 41 per cent levied on savings, while some may have to pay an additional 4 per cent PRSI charge. And the bad news is this situation is unlikely to change in the short-term, as stagnant European growth and elevated debt levels conspire to keep interest rates at historic lows.

“Our view in this environment is that we’ll see negative interest rates for a prolonged period of time,” says Quigley. “There is a lot of debt in the world and the most ‘effective’ way of tackling this debt is for governments to be able to fund their borrowings at very low interest rates for a very long time. This is what happened in the decades following the last great build up in debt after the second World War and history is clearly repeating itself.”

The result is a transfer of wealth from savers to borrowers to allow the economy rebalance.

Inflation targets

However, in the relative absence of inflation, savers have escaped a loss in the real value of their wealth. In October, inflation stood at just 0.4 per cent in the Eurozone for example, and just 0.2 per cent in Ireland. Last month, the Irish rate fell to 0.1 per cent, but the risk now is that inflation is primed to rise. In November,

European Central Bank

president

Mario Draghi

told the markets that inflation is firmly back on the ECB’s agenda, as it strives to stimulate growth in Europe.

“It is essential to bring back inflation to target and without delay,” he said. The European target of course is 2 per cent, which could eat into Irish savers’ already meagre returns, and start to erode their capital.

Described as the “silent thief”, inflation reduces the “real” or purchasing power of your capital. “To lose 1 per cent in real terms per annum doesn’t seem that destructive to your wealth,”says Quigley, but he notes that if you compound it for a long time, it can really hurt your capital.

Consider the impact of inflation on a €50,000 deposit. If you take whatever interest you earn as income, inflation at 2 per cent will reduce your capital to just €45,200 in real terms at the end of five years. Push it out over 10 years, and in terms of purchasing power, you’ll have lost almost €10,000.

Joe Hanrahan, head of personal financial services at Investec, sums up the quandary facing savers as such: "if I leave it on deposit I will lose purchasing power for a long period of time, so I'm compelled to do something else with my money".

“Irreplaceable capital”

And the unusual interest rate environment poses a further challenge, coming as it does at a time when many Irish individuals and families are finding themselves forced into the realm of investment.

A move away from defined benefit (DB) type pensions and away from annuities to approved retirement funds, puts the focus on the individual providing for themselves, which means that Irish savers are increasingly having to consider themselves as investors.

“It’s a seismic shift,” says Hanrahan, noting that most people in Ireland never had enough discretionary income or capital to invest. Indeed unlike the US, Ireland does not have a history of an equity owning culture – and those who have invested in Irish stocks have been chastened by the experience. “Many DB schemes are winding up, so we’re now dealing with ordinary individuals who have never had to worry about investing,” he says.

Quigley uses the term “irreplaceable capital” to describe the challenge facing many people in such a position.

Either at, or near, the end of their working life, if they lose their capital, they will have no means of replacing it.

So, while a transfer value of €300,000-400,000 might seem enormous, if it is eroded, such individuals will have nowhere else to turn to fund their retirement.

In this respect, leaving all their money on deposit may be a risk.

“The damage may already have been done in an under-funded DB scheme, and you could compound that error again,” says Hanrahan.

Plan your portfolio

So what’s the solution?

“Generally my advice is to say – ‘leave the amount of money in cash that you think you’ll need’,” says Quigley, adding that it may be a case of determining the amount of money you need “emotionally”, rather than financially.

This money should be placed in the highest yielding accounts you can find. With the rest of your money, you can work out how it should be invested, how it should be diversified – and how much risk you are inclined to take.

While Quigley acknowledges that Irish investors may have a “jaundiced view of equities”, he says that opting for high-quality assets, where valuations are reasonable, is a good route to go.

“If you buy assets that have a sustainable and growing income – that type of diversification makes a lot of sense.”

Structured products, which guarantee your capital but assume an element of risk which means you might get a better return, can be popular but Hanrahan says that in a low interest rate environment, Hanrahan says it may be the “wrong time to buy them”.

It’s also wise to approach new investment structures with caution.

“When interest rates are very low, and you’re starved of income, new investments might be a bit questionable,” says Quigley, noting that if it works out, you may not have noticed the risk you were taking to get that return.

Finally, it’s not enough to just invest and walk away – your portfolio needs consideration at regular intervals.

“Critically, it needs ongoing stewardship,” says Hanrahan, noting that the concept of buying a managed fund and staying invested in it over the long-term is “bonkers”. “People change, circumstances change – you could find you’re totally misallocated.”

Next week: If you’re looking to get a better return on some of your savings, we round up the best – and worst – performing funds of the year