Haruhiko Kuroda, the new governor of the Bank of Japan, has launched a monetary policy revolution. He has ended two decades of caution, during which the BoJ declared itself helpless to end deflation. Prime Minister Shinzo Abe's goal of 2 per cent inflation within two years is ambitious – and Kuroda now has a bold policy to meet it. The question is whether the policy will work. My answer is: on its own, no. The government must follow up with radical structural reforms.

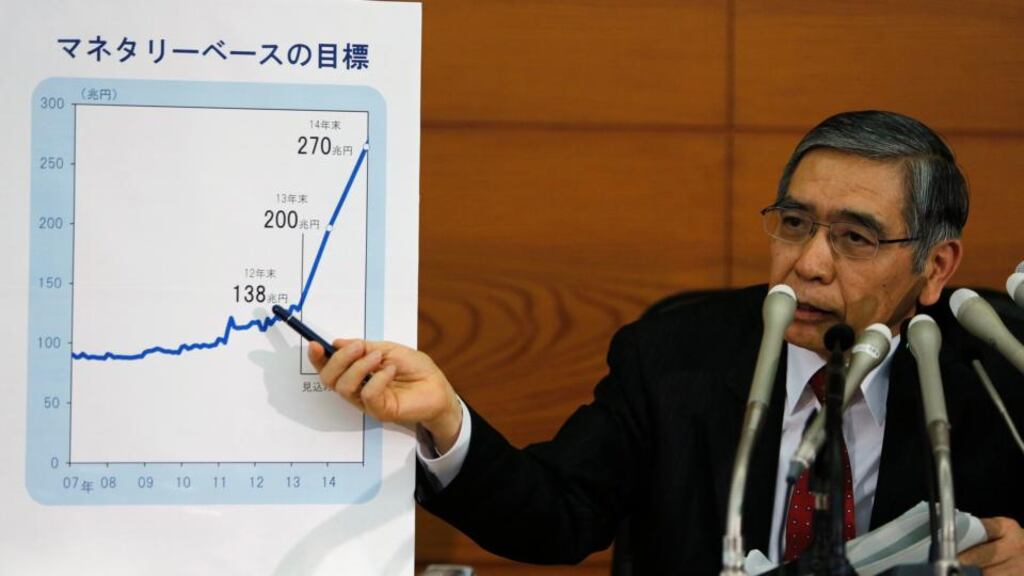

On April 4, the Bank of Japan announced the launch of “quantitative and qualitative easing”. It promises to double the monetary base and to more than double the average maturity of the Japanese government bonds that it purchases. The monetary base will rise at an annual rate of Y60 trillion-Y70 trillion ($600 billion–$700 billion or 13-15 per cent of gross domestic product) and the average maturity of holdings of JGBs will increase from three to seven years. Furthermore, says the BoJ, it “will continue with the quantitative and qualitative monetary easing . . . as long as it is necessary”.

This is not "helicopter money", since the intention is to reverse the monetary expansion when the economy recovers. This is also not an outright purchase of foreign assets, as the Swiss National Bank has done. This is, instead, in the words of Gavyn Davies, chairman of Fulcrum Asset Management, "an outsize dose of internal balance sheet manipulation", designed to encourage the financial sector to shift from holdings of JGBs and to raise the prices of real assets. Nevertheless, a weaker exchange rate is surely a desired consequence.

Why might this work? The answer is that Japan suffers from a structural excess of savings in the private sector. Companies are accumulating too much cash. The announced policy could change this, at least temporarily, in a combination of two ways. First, by lowering the real exchange rate, it could increase Japan’s ability to export excess savings via a larger current account surplus. Second, by turning the real interest rate negative and also raising real wealth, the policy might raise investment and lower savings.

Structural obstacle

Yet, at best, this would only work in the short run. At worst, it could destabilise inflation expectations so dangerously that it pushes Japan from deflation to ultra-high inflation, without stopping for long at any point in between. Thus, the Japanese might decide that the aim of the government is to impoverish them brutally, by reducing the real value of their (admittedly unsustainable) savings. If this frightened them into fleeing the yen, policymakers would be at a loss, since they could not respond by increasing interest rates without devastating the public finances. They might even have to impose exchange controls.

What, then, has to be done to make the shift in monetary policy work? The answer is to recognise that the underlying obstacle is structural: it lies in what is now a dysfunctional corporate sector.

Andrew Smithers of Smithers & Co and Charles Dumas of Lombard Street Research have made much the same point. Japan's private savings – almost entirely generated by the corporate sector – are far too high in relation to plausible investment opportunities. Thus, the sum of depreciation and retained earnings of corporate Japan was a staggering 29.5 per cent of GDP in 2011, against just 16 per cent in the US, which is itself struggling with a corporate financial surplus.

As Dumas notes, US gross fixed business investment has averaged 10.5 per cent of GDP over the past 10 years, against Japan’s 13.7 per cent. Yet US economic growth has much exceeded Japan’s. Japanese corporations must have been investing too much, not too little. It is inconceivable that raising the investment rate, to absorb more of the corporate excess savings, would not add to the waste. In the short term, negative real interest rates might raise investment a little, since savings earn less. But, in the medium to long term, Japanese corporate investment should fall. Since household savings are low and their willingness to borrow is small, this leaves only two other areas capable of absorbing the huge excess savings of the corporate sector: foreigners and the government.

In practice, the government has largely done the job over the past two decades. That is why fiscal deficits are huge and public sector indebtedness is ever rising. Meanwhile, the external surplus has diminished. This is due to worsening terms of trade and poor performance on export volume. Again, a depreciation in the yen should help, but only a little. The current account surplus needed to absorb the excess savings of the corporate sector and generate the fiscal surplus needed to lower public debt ratios would be at least 10 per cent of GDP. Still a fairly closed economy, Japan could not generate such a surplus. If it could, the rest of the world would surely not absorb it.

It follows that Japan desperately needs structural reform – but not just any structural reform. It needs reform that both lowers excess corporate savings and increases the trend rate of economic growth. This combination should be possible, since Japan’s GDP per head (at purchasing power parity) is down to 76 per cent of US levels and its GDP per hour to just 71 per cent. The policy options include: a huge reduction in depreciation allowances; a punitive tax on retained earnings, possibly combined with incentives for higher investment; and reform of corporate governance, to give more power to shareholders. The aims would be to deprive companies of the cash flow cushion that has featherbedded inefficiency. The worst possible tax rise is the one on consumption now planned, since Japan consumes too little. Tax corporate savings, instead.

Lessons for China

Such reforms really would be radical. Is there the smallest chance that Abe might move in this direction? No. But without this sort of reform, the BoJ's new policy will prove, at best, a short-term palliative and at worst an inflationary disaster. Meanwhile, China needs to note that this is the end result of an economy built by favouring investment and suppressing consumption. That is a great strategy for catching up with the rich world, but it leaves huge headaches when fast growth is over.

– Copyright

The Financial Times Limited 2013