The best thing that can be said for Brexit is that it is a teachable moment: an admittedly very expensive, but also very useful, civics lesson on a grand scale.

Those who will learn the most are in Britain, but the rest of us will also benefit. And there is a considerable upside to that, especially on the periphery of the euro zone.

Like many but by no means all mainstream economists, I was never very keen on the euro – the profession is genuinely split on the issue. We all agree that it provides a variety of benefits, and most of us agree that it also involves costs: a one-size-fits-all monetary policy, an inflexible exchange rate, and a “banking union” that is not fit for purpose.

Where we disagree is about the relative importance of these costs and benefits, I have always been of the opinion that the former outweigh the latter, and that the recent euro-zone crisis demonstrated this in rather dramatic fashion, but others whom I respect take the opposite point of view, and always will.

In sharp contrast, there is no disagreement whatsoever among mainstream economists about the EU customs union and single market. We all agree that both have been hugely beneficial to Ireland, and are essential for its continuing prosperity.

We don’t think this because economic theory tells us so, although it does. Rather, Ireland’s economic history is such that it is impossible to think otherwise.

Ireland’s accession to the then EEC in 1973, and the construction of the single market in the early 1990s, were the two crucial turning points that allowed our Republic to put decades of underachievement behind it and become the prosperous and self-confident State that it is today.

Brexit will forcibly remind us of these core benefits of EU membership.

More benign

I don't share the view that Irish economic policymaking since independence was an unmitigated disaster. In particular, our interwar economic policies were entirely typical for the period, and were in many respects more benign than those pursued elsewhere. However, there can be no doubt that our economic performance between 1950 and 1973 – decades which in France are remembered as the Trentes Glorieuses, and in Germany as the Wirtschaftswunder – was very poor.

Take a look at the graph, which gives a snapshot of economic growth in western Europe and the United States between 1954 and 1973. On the horizontal axis, I have plotted countries' incomes per capita in 1954. Initially rich countries such as the US are on the right hand side of the graph, while initially poor countries such as Greece and Portugal are on the left. On the vertical axis, I have plotted the average annual per-capita growth rate achieved by these countries over the course of the subsequent 19 years.

Poor countries

As you can see, these two variables are negatively related to each other: during this period, initially poor countries, such as Greece, Portugal and Spain, grew much more rapidly than initially rich countries such as Switzerland and the US. In other words, this was a period that saw economic convergence, on average, in western Europe.

In that context, Ireland was a spectacular underperformer. It grew slightly less rapidly than Switzerland, despite being poorer than Italy. To be sure, it grew faster than the United Kingdom, but growing faster than the sick man of Europe was nothing to be proud of. While we might have been gradually catching up on Britain during this period, we were falling further and further behind France.

Strikingly, the graph shows that Scotland, Wales, and Northern Ireland were also underperformers during this period; they and we were all hampered by an excessive dependence on a sluggish and crisis-prone British economy.

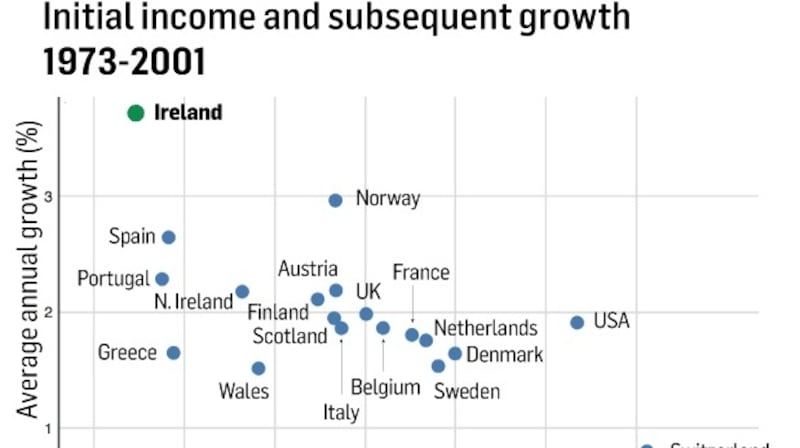

Everything changed as soon as we joined the EEC in 1973. We immediately stopped falling further behind France, and started growing at a normal European rate. We were now growing about as fast as we should have been, given how poor we were in 1973.

That was true even if you consider the fairly dismal years 1973-1990: Ireland was no longer an underachiever in the western European context. Foreign direct investment, based on selling into the EEC, was the major factor improving Irish performance from 1973 onwards, although the Common Agricultural Policy clearly also helped. We would have done even better had it not been for the budgetary mistakes of the late 1970s, and their inevitable consequences in the succeeding decade.

As we know, Ireland became a spectacular overachiever following the domestic reforms of the late 1980s, social partnership, and the creation of the European single market.

The contrast between our performance before (figure 1) and after (figure 2) 1973 could not be starker.

Foreign direct investment (FDI) premised on our membership of the European single market was the key to our eventual success, and membership of the single market remains our greatest economic asset going forward.

Corporate tax

The English nationalists driving Brexit don’t care about any damage that their project may do to Ireland, North or South, but that doesn’t stop them from occasionally suggesting that Ireland would do well to come home to the fold, and join them in their exile.

Their fellow travellers here opine that we should “seriously consider” the matter, perhaps because our corporate tax rate may eventually come under threat.

But consider this: our corporate tax rate only helps because it gives companies a competitive platform inside the EU. And the notion that Ireland, outside the EU, could negotiate a deal with the EU26 that granted them access to our huge domestic market, in return for our continuing to act as a low-tax FDI platform exporting to the rest of Europe, is absurd even by Brexiteer standards.

Brexit is making us all appreciate the economic benefits of the EU customs union and single market, and that is good. For whatever we may think about the euro, or the EU’s democratic deficit, or any of the other problems currently bedevilling Europe, the single market is an extraordinary achievement. Look at how it has erased the economic border within this island despite the lack of a single Irish currency, I can’t help but noting!

And look at how Northern Ireland’s exit from the customs union and single market, should it happen, will cause that border, inevitably, to return.

But even more importantly, Brexit is making us appreciate the freedoms which we all enjoy, to study, live, work, and retire wherever we want in this wonderful continent of ours. We take those freedoms for granted, but there is nothing natural about them at all.

Distraught

You only really appreciate the value of European citizenship when you see how distraught many Britons are at losing it. And the commitment to the international rule of law that the EU epitomises is more important today than it ever was. Aside from the clear economic benefits of EU membership, this is a project that is worth buying into for its own sake.

And that is a final lesson to be learned from Brexit. The English were always in the EU primarily for what they could get out of it, and that transactional attitude finally cost them dearly. We mustn’t make the same mistake.

Kevin Hjortshøj O’Rourke is Chichele professor of economic history at the University of Oxford and a fellow of All Souls College