Growth in the Irish economy will slow significantly next year as high inflation and low confidence weigh on consumer spending, the Organisation for Economic Co-operation and Development (OECD) has warned.

The Republic will, however, avoid an all-out recession, with “resilient” multinational exports from the pharma and medtech sectors continuing to fuel growth, it said.

In its latest economic survey of Ireland, the Paris-based agency predicted falling real incomes due to inflation would hold back consumer spending in 2023 despite significant wage growth.

At the same time, high costs and low confidence would reduce companies’ incentives to invest.

RM Block

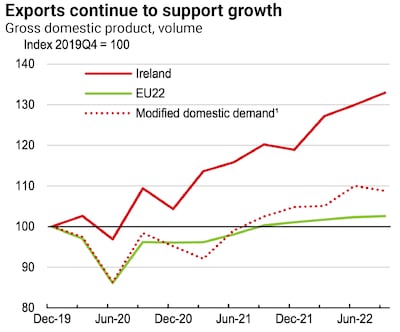

It forecast that gross domestic product (GDP) and modified domestic demand, the two most commonly used measures of economic growth here, would grow by 3.8 per cent and by 0.9 per cent respectively in 2023, down from 10.1 per cent and 8 per cent this year. These forecasts are also subject to significant downside risks given the uncertainties surrounding Russia’s war in Ukraine.

The OECD said the reopening of the Irish economy after Covid had triggered a strong bounce-back in activity, but inflationary pressures have emerged since then. Irish GDP is now a “mind-boggling” third bigger than it was before the pandemic and modified domestic demand is more than 9 per cent greater, Vincent Koen, deputy director of the country studies branch of the OECD economics department, noted at an event at the Institute of International and European Affairs (IIEA) in Dublin on Wednesday.

“I can’t think of any other OECD country in this league,” Mr Koen said of the Irish GDP, which the Government estimates will amount to almost €500 billion this year and has been underpinned by multinationals based in the State.

The OECD warned that high inflation, while still driven by elevated energy prices, had become more broad-based, especially through higher transport and service costs.

Inflation is expected to average 8.4 per cent this year, before falling to 7.2 per cent next year and to 2.9 per cent in 2024.

“The Irish economy weathered the Covid-19 pandemic and is coping well with the repercussions from Russia’s war of aggression against Ukraine,” the agency said.

It said the Government “reacted forcefully” to shield households and businesses from both shocks while buoyant exports from the multinational sector and very high vaccination rates helped the economy to recover strongly when the strict lockdown was lifted.

While Irish trade links with Russia are modest, the OECD noted that the State had become an international hub for special-purpose vehicles engaged in aircraft leasing and that the war would have a sizeable impact on the Irish aircraft leasing industry, which manages more than €100 billion in assets.

About 150 planes are rented to Russian airlines and there are significant uncertainties around recovering these aircraft from Russia, it said.

Separately, it said excess corporate tax receipts would push the budget “back into balance” in 2022, despite substantial Government supports being deployed to deal with the cost-of-living crisis.

While high inflation was putting pressure on the Government to spend more, a new 5 per cent spending rule was an attempt to make “spending less pro-cyclical”.

Nonetheless, there were “several underlying pressures” that posed threats to fiscal sustainability in the future, including more rapid population ageing, which will push up health costs. The agency also noted that the State’s climate change objectives would require significant additional spending.

The report highlighted that plans to raise the State pension age had been abandoned while the recent multilateral agreement on corporate taxation could reduce the buoyancy of receipts, “although effects are very uncertain”.

The outgoing Minister for Finance, Paschal Donohoe, told reporters after the IIEA event that there were no plans to revisit the pension age, after the Government decided this year that it will stay at 66. However, he said the pensions system should be put on a more sustainable footing by “reaching a decision regarding the right level of PRSI within our tax code”.

Meanwhile, the Minister said that the Government will legislate in the next budget for a 15 per cent corporate tax rate, after the EU reached agreement this week that this become the minimum taxation rate for large companies across the bloc, under reforms being championed by the OECD.

On climate change, the OECD said the Republic did not meet its 2020 emissions reduction target and had among the highest greenhouse gas emissions per capita in the OECD “partly due to the importance of agriculture”.

The agriculture sector presents particular difficulties for abatement, it said.

“Achieving methane emission reductions has proven to be difficult and the dairy herd has actually been growing, making the targets even more difficult to reach,” it said.